How fintech innovations are accelerating the energy transition

Though not always included in conversations around climate tech, finance is an essential component of the energy transition. Most of the sustainable infrastructure projects that form the energy transition’s backbone require financial lending, from large scale solar and wind projects to heat pumps in residential homes. Climate-related finance is a multi-decade trend that has continually required financial technology (fintech) innovations. As we transform our physical energy assets from traditional to renewable energy sources and create emerging environmental markets – such as carbon credits and energy credits – our financial mechanisms have likewise needed to adapt and innovate.

For example, the energy transition would arguably not be possible without the creation of renewable energy project finance structures. Instead of relying solely on long-term debt financing, project finance structures allow investors to finance renewable energy projects through a combination of equity, debt and tax credits. Power Purchase Agreements (PPAs) have further unlocked financing for the construction and operation of renewable assets – since renewable energy projects have higher upfront capital costs but lower operating costs, PPAs can provide a more stable and predictable revenue stream for the power generator, making it easier to secure financing for wind and solar projects.

Time and time again, traditional financial markets and mechanisms have innovated – slowly, then all at once – to offer different mechanisms to transfer risk, improve liquidity and access credit for sustainability-based projects. And this is just the beginning; we believe massive opportunities for iteration and innovation will emerge as we continue to build and optimize the capital channels needed to support sustainable asset flows.

For the last two and a half years, members of the Energize team have been developing a thesis at the intersection of fintech and climate, from the financial infrastructure powering carbon markets to contractor revenue platforms. Our work has been guided by our proprietary research backed by our team’s prior experiences at leading financial institutions such as JPMorgan and Morgan Stanley. Our overarching fintech x climate investment thesis is simple. We believe fintech solutions can help remove financing soft costs and reduce investor risk, enabling both:

1) Increased flows of capital in the climate space

2) More efficient capital workflows

In short, we believe software can help power a new wave of innovation in climate-related finance by enabling more effective financing processes. As part of our work in this space, we’re charting the issues creating barriers to climate action as well as the fintech innovations that are helping surmount them. For example:

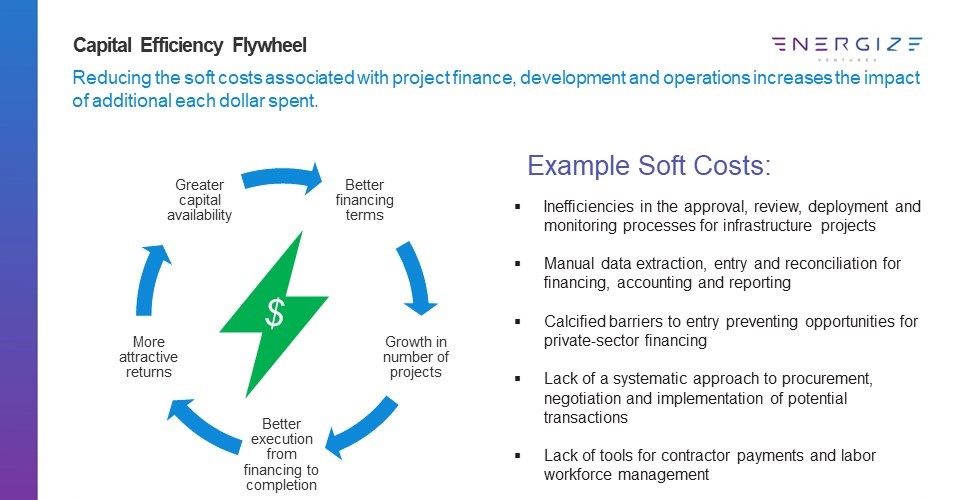

1) Reducing soft costs and automating inefficient processes.

- The issue: Much of the energy transition’s financing is managed with legacy tools – such as Excel—and manual workflows, and the resulting inefficiencies are standing in the way of large-scale climate action. Soft costs like accounting and compliance make up roughly one-third of the total price tag for solar projects, creating bottlenecks and friction that inhibit some investors from wanting to invest in the energy transition at all.

- The innovation: Software solutions are pulling sustainable infrastructure project finance from the dark ages by automating transactions and helping standardize and accelerate financiers’ due diligence processes. Software platforms like Banyan Infrastructure, an Energize portfolio company, are removing soft costs and helping financiers of all sizes manage financing workflows for sustainable projects more efficiently, allowing more capital to flow into the space.

2) Managing complex renewable energy project transactions.

- The issue: Renewable energy projects are priced fundamentally differently than, say, the funding of a coal power plant – they have nuanced clauses, calculations and complications, making the workflows for legal structuring, underwriting, financing and securing contracts difficult to scale. While financial options such as PPAs help renewable developers manage market price risk, they may also increase project complexity and underlying credit risk.

- The innovation: Software solutions are stepping up to help make renewable energy project financing feasible at scale. For example, climate software companies like Pexapark are changing the way PPAs are tracked and traded through the system by providing an operating system platform for buying, selling and managing renewable energy. Companies like Perl Street are making it easier to bundle finance solutions for hardware-intensive deployments of distributed assets, unlocking additional capital through special purpose vehicles (SPV) as financing structures.

3) Bringing greater transparency to voluntary carbon markets.

- The issue: Carbon credits enabling reduction, removal and avoidance of carbon emissions are an essential tool in fighting climate change, and demand for credits is growing exponentially as corporates chase net-zero goals. Yet voluntary carbon markets have been mired in mistrust and confusion due to concerns around carbon credit quality, leaving many potential buyers on the sidelines.

- The innovation: By tokenizing carbon credits, blockchain solutions can improve credits’ reliability (see the Rocky Mountain Institute’s 101). Several new blockchain players in the space, such as Toucan, have been pushing voluntary carbon markets towards a digital renaissance, and carbon credits incumbents have been following suit by scaling up their own digital strategies. While market adoption is still early, we believe blockchain solutions can be instrumental in improving traceability, liquidity and overall accountability within voluntary carbon markets – which can in turn be crucial for capping carbon emissions.

4) Accessing capital for the energy transition.

- The issue: Finally, the current banking crisis has spiked anxiety around the ability of emerging industries – like climate tech – to source capital. While utility scale projects have been able to tap infrastructure investors for capital, smaller distributed assets often don’t have the volume or visibility sought by most institutional investors. Silicon Valley Bank (SVB) had helped fill the capital gap by serving as a frequent lender for renewables projects, and the bank’s collapse has caused rising concerns among the energy community that it could become more difficult for sustainability projects to secure much-needed funding.

- The (need for) innovation: As with previous bank failures, the reckoning prompted by SVB’s collapse can help create a wedge for more lending and underwriting solutions to emerge. At Energize, we view this banking sector setback as a major moment for fintech x climate innovation. We believe fintech solutions – such as Enduring Planet’s climate-focused rapid financing and Spring Free EV's electric vehicle-focused financing – can step in to help reduce investor risks and facilitate financing for clean energy projects. Where there is crisis, there is opportunity!

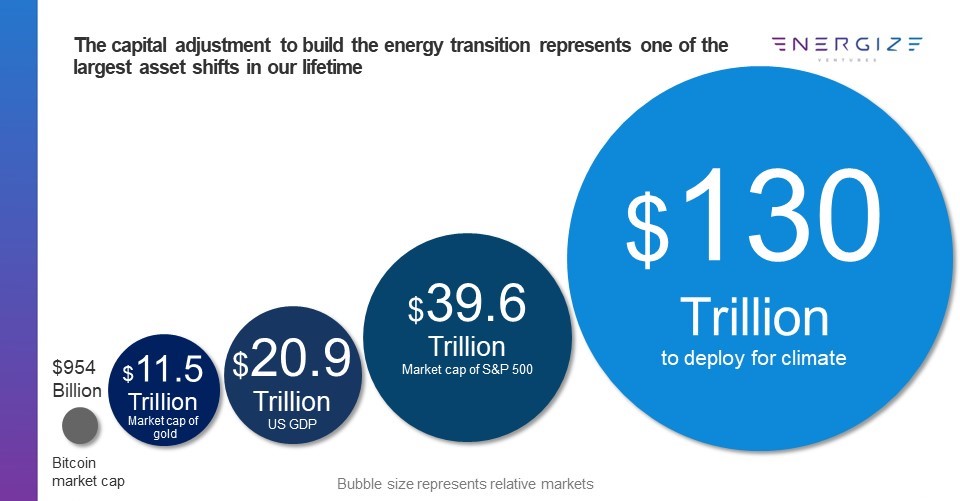

We believe this is only the beginning of the explosion of fintech innovation we are about to see – and it will be needed to keep pace with the flourishing climate tech market. Capital investments in the renewable energy sector are now outpacing deployments in new oil and gas developments, with more than 70 percent of investments in new power generation going to renewables. As the global power generation mix shifts to renewable power, trillions of dollars will need to be deployed to finance the energy transition.

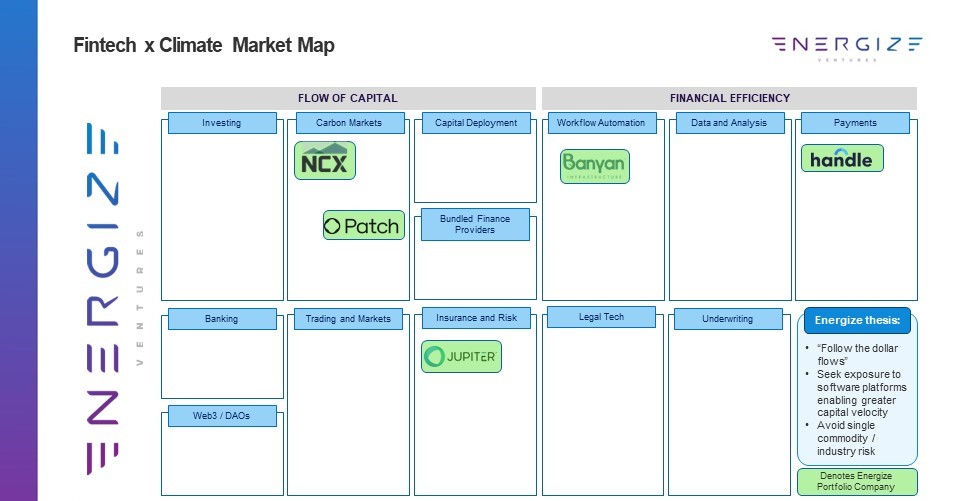

Energize is continuing to explore the next generation of market development tools aimed at improving the flow of capital to the energy transition and the financial efficiency of the assets deployed. We’re sharing our market map (below) that highlights each of the major verticals driving innovation within climate fintech, and we’ll continue to share our market insights. Stay tuned!

This article represents the views of the author and is provided for informational purposes only. It is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Readers should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Information is subject to change based on market or other conditions.

Recent News & Insights

Let’s Build What’s Next